Table of Contents >> Show >> Hide

- Quick Definitions (So We’re Speaking the Same Financial Language)

- Money Order vs. Cashier’s Check: The Core Differences

- Limits: How Much Can You Send?

- Cost: Fees, Purchase Price, and “Surprise” Expenses

- Where to Buy Them (and What You’ll Need)

- Speed and Funds Availability: Why “Guaranteed” Still Doesn’t Mean “Instant”

- Security and Scam Risk: The Unfun Part You Really Should Read

- Cancellation, Replacement, and “Help, I Lost It” Scenarios

- Which One Should You Use? Real-Life Examples

- Decision Checklist (Fast, Practical, No Overthinking)

- FAQs

- Final Take

- Real-World Experiences: What People Learn the First Time They Use These

- Experience #1: The “Rent Payment Puzzle”

- Experience #2: The “I Need $2,200… But the Limit is $1,000” Moment

- Experience #3: The “Buying a Used Car Without Carrying a Backpack of Cash”

- Experience #4: The Scam Story That Changes How People Receive Payments

- Experience #5: The “Why Did They Ask for My ID?” Surprise

Need to pay someone without handing over a wad of cash that makes you feel like you’re starring in a low-budget heist movie?

Two classic options are money orders and cashier’s checks. They’re both widely accepted, more secure than cash,

and (usually) less dramatic than trying to Venmo your landlord who “doesn’t trust apps.”

But they’re not twins. They’re more like cousins who show up to the same family barbecue wearing totally different outfits:

money orders are generally easier to buy and have lower limits, while cashier’s checks handle bigger amounts and can feel “more official.”

Let’s break down limits, costs, safety, and real-world tradeoffs so you can pick the right tool for your payment job.

Quick Definitions (So We’re Speaking the Same Financial Language)

What is a money order?

A money order is a prepaid payment instrument. You pay the issuer upfront (plus a fee), and the money order is issued for a specific amount to a specific payee.

It’s popular when someone needs a guaranteed form of payment but you don’t want to mail cash or you don’t have a checking account.

What is a cashier’s check?

A cashier’s check is issued by a bank (or credit union) and typically draws on the bank’s funds rather than your personal checkbook.

In practice, your bank verifies you have the money (or you provide the money), then the bank issues the check, which many recipients treat as more secure for larger payments.

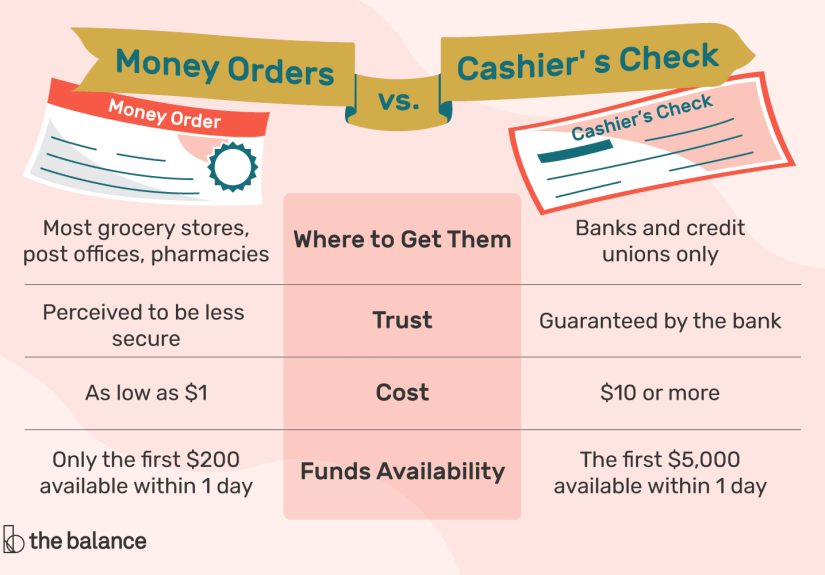

Money Order vs. Cashier’s Check: The Core Differences

| Feature | Money Order | Cashier’s Check |

|---|---|---|

| Typical max amount | Often up to $1,000 per money order (varies by issuer) | Often higher amounts; limits depend on bank policy and your funds |

| Where you get it | Post office, retailers (e.g., big-box stores), some banks/credit unions | Banks/credit unions |

| Typical cost | Usually low (often around $1–$5), depends on issuer | Often around $10–$15, may be waived for some customers |

| Best for | Smaller payments, paying bills, rent, sending money safely | Larger payments (car purchase, closing costs), “official” transactions |

| Risk of fraud | Can be counterfeited; verify before accepting | Can be counterfeited too; “looks official” doesn’t mean it is |

Limits: How Much Can You Send?

Money order limits (the “small but mighty” option)

Money orders commonly have relatively low maximum values per instrument.

A major example: USPS domestic money orders can’t exceed $1,000 each.

If you need to pay $2,400, you may be buying multiple money orders and feeling like you’re collecting trading cardsexcept the hobby is “rent.”

USPS also lists limits for international postal money orders where available: up to $700 (with lower limits for certain destinations).

Policies can vary by issuer and country availability, so always confirm before you plan a payment around it.

Many retailers that sell money orders also keep limits around the same general neighborhood (often $500–$1,000 per money order).

You can usually buy multiple money orders, but if your total is large, expect extra scrutiny, extra recordkeeping, and possibly ID requirements.

Cashier’s check limits (the “bigger league” option)

Cashier’s checks typically support higher dollar amounts because they’re issued by banks and backed by verified funds.

That said, banks can still have policies that affect youespecially if you’re ordering online versus in person.

For example, some banks allow online cashier’s check orders only up to certain thresholds, with higher amounts requiring a branch visit.

Practical rule: if you’re paying several thousand dollars or more and the recipient wants one clean payment instrument (not three money orders and a sticky note),

a cashier’s check is often the smoother path.

Cost: Fees, Purchase Price, and “Surprise” Expenses

Money order costs

Money orders are usually inexpensive. Two real-world anchors:

-

USPS money order fees depend on the amount (for example, one fee tier up to $500 and another up to $1,000).

The post office is a great option when you want a widely trusted issuer and clear pricing. - Walmart money orders (powered by a major issuer) advertise a maximum fee of $1 in many locationsoften one of the cheapest mainstream options.

Possible “hidden” costs: some places charge to cash money orders (especially if you don’t have an account there),

and replacing a lost money order can involve paperwork and processing fees. Translation: keep your receipt like it’s the last cookie in the jar.

Cashier’s check costs

Cashier’s checks generally cost more than money orders, but the fee is often predictable.

Many major banks charge around $10–$15, and some waive fees for certain account tiers or relationship customers.

Also note: banks may charge extra for delivery if you request a cashier’s check by mail or through certain online ordering options.

If you need it today, getting it in person can be cheaper and faster.

Where to Buy Them (and What You’ll Need)

Where to buy a money order

- USPS (post offices)

- Retailers (some big-box stores, grocery stores, and pharmacies)

- Money transfer providers through partner locations

- Some banks/credit unions

You generally pay with cash or a debit card (varies by location), fill in the payee name, and keep the stub/receipt.

For larger purchases, you may be asked for ID. There are also federal recordkeeping rules that can apply when purchasing certain monetary instruments with cash in the

$3,000–$10,000 range, and large cash transactions can trigger additional reporting requirements.

Where to get a cashier’s check

- Your bank or credit union branch (most common)

- Some banks’ online banking (often with amount limits or delivery options)

Typically, you’ll need an account (or at least funds) and identification. The bank will either debit your account or require you to provide funds, then issue the check payable to the recipient.

Speed and Funds Availability: Why “Guaranteed” Still Doesn’t Mean “Instant”

People love cashier’s checks and money orders because they feel “safer” than personal checks. That’s often true.

But here’s a plot twist: banks can still place holds on deposited funds, especially if something seems off.

Under federal rules (Regulation CC / Expedited Funds Availability), certain itemslike cashier’s checks and some government-related instrumentscan qualify for faster availability rules,

but there are exceptions and safeguards for banks. In plain English: your recipient’s bank may still wait to make funds fully available if it suspects fraud or if the deposit triggers certain risk conditions.

If you’re the one receiving a cashier’s check for a marketplace sale, don’t assume “it cleared” just because your banking app shows the deposit.

Scams thrive in that gap between “funds appear” and “funds are actually final.”

Security and Scam Risk: The Unfun Part You Really Should Read

Yes, cashier’s checks can be fake

Counterfeit cashier’s checks are common in fraud schemesespecially overpayment scams.

The check looks real, the buyer “accidentally” sends extra, and asks you to refund the difference quickly. Later, the bank determines the check is fake and reverses the deposit.

Now you’re out the refunded money. The scammer is gone. Your stomach falls through the floor. Classic.

Money orders can be counterfeited too

Money ordersespecially those from trusted issuersinclude security features and verification steps. USPS, for example, publishes guidance on how to spot fake postal money orders,

including details like watermarks and signs of tampering.

How to protect yourself (without becoming a full-time detective)

- Use trusted issuers and buy directly from them or reputable partner locations.

- Verify before you accept (especially if you’re receiving a cashier’s check or money order from someone you don’t know).

- Never refund “extra” money until you’re certain the payment is legitimate and final.

- Keep receipts and documentationthey matter for tracking, disputes, and replacements.

Cancellation, Replacement, and “Help, I Lost It” Scenarios

If you lose a money order

Replacement is often possible if you have your receipt and details (serial number, amount, purchase location/date).

The process varies by issuer and may involve fees and a waiting period. The key is: the receipt is your proof that you bought it and your ticket to start a trace.

If you lose a cashier’s check

This can be more complicated. Banks may require a stop payment request, paperwork, and sometimes an indemnity agreement (or bond) depending on the situation and the bank’s policy.

If you’re using a cashier’s check for a major purchase, treat it like cash: secure it, track it, and hand it off carefully.

Which One Should You Use? Real-Life Examples

Use a money order when…

- You’re paying rent or a bill and the amount is within common money order limits (e.g., $300–$1,000).

- You don’t have a bank account or don’t want to use personal checks.

- You want a low-fee, widely accepted payment option.

Example: You owe $850 for rent and your landlord only accepts “guaranteed funds.” A USPS money order works nicelyone instrument, clear receipt, and a known issuer.

Use a cashier’s check when…

- You’re making a large payment (car purchase, home-related costs, big contractor deposit).

- The recipient wants one clean payment instrument (not multiple money orders).

- You want the perceived credibility of a bank-issued instrument.

Example: You’re buying a used car for $11,500. A cashier’s check is typically more practical than showing up with 12 money orders and an awkward grin.

Decision Checklist (Fast, Practical, No Overthinking)

- Amount under $1,000? Money order is often easiest and cheapest.

- Amount several thousand or more? Cashier’s check is usually cleaner.

- No bank account? Money order wins on accessibility.

- Worried about scams? Either can be fakedverification and patience matter more than the instrument type.

- Need a paper trail? Both provide onejust keep your receipt/stub and document the transaction.

FAQs

Is a cashier’s check safer than a money order?

For large transactions, cashier’s checks are often preferred because they’re bank-issued and backed by verified funds.

But both can be counterfeited, so “safer” depends heavily on whether you verify and follow smart anti-scam practices.

Can I buy a money order with a credit card?

Many places don’t allow credit cards for money orders because it can resemble a cash advance. Policies vary by location, so ask before you get to the register and hold up the line.

Can someone track a money order or cashier’s check?

Many issuers provide tracking or verification options if you have the serial number and purchase details. Tracking is one reason these instruments beat sending cash in the mail.

What if the recipient refuses multiple money orders?

This happens, especially for large purchases. Some recipients don’t want the hassle of depositing several instruments.

That’s a strong sign to switch to a cashier’s check (or another method the recipient prefers).

Final Take

If money orders and cashier’s checks were shoes, money orders would be your dependable sneakers: affordable, easy to get, great for everyday payments.

Cashier’s checks would be your dress shoes: a bit pricier, more formal, and built for big moments (like buying a car or handling a serious deposit).

Pick based on amount, cost, access, and recipient expectations.

And no matter which you use, keep your receipt, verify payments when receiving them, and don’t let urgency bully you into a scam.

=========================================================

EXTRA 500+ WORDS: EXPERIENCES SECTION (FOR LENGTH + UX)

=========================================================

Real-World Experiences: What People Learn the First Time They Use These

Most people don’t think about money orders or cashier’s checks until life drops a very specific task in their laplike “pay a security deposit by Friday”

or “bring certified funds to the title transfer.” Then suddenly you’re comparing fees, limits, and office hours like it’s your new hobby.

Experience #1: The “Rent Payment Puzzle”

A common first money order experience is paying rent when a landlord won’t accept personal checks. The plan sounds simple: buy a money order, hand it over, done.

The learning happens in the details. People often realize they need the exact payee name, and they learn quickly that writing the wrong name can turn a five-minute errand into a paperwork saga.

Another practical lesson: the receipt/stub is not “junk.” It’s your proof of payment. Folks who toss it often wish they hadn’t when a landlord says,

“I don’t see it on my end.” The people who keep it? They calmly provide the serial number and feel like financial superheroes.

Experience #2: The “I Need $2,200… But the Limit is $1,000” Moment

Money order limits are where reality taps you on the shoulder. Someone might need to pay a contractor deposit of $2,200 and think,

“Money orders are safe. I’ll just get one.” Then they meet the per-instrument cap. Suddenly, they’re buying three money orders, triple-checking amounts,

and carrying multiple slips of paper like they’re transporting a fragile document collection.

This is also the moment people discover that some recipients dislike multiple money orders.

It’s not personal; it’s inconvenience. Depositing three instruments instead of one can mean extra time at the bank, extra tracking, and more room for errors.

When that happens, switching to a cashier’s check feels like upgrading from “three separate puzzle pieces” to “one solid block.”

Experience #3: The “Buying a Used Car Without Carrying a Backpack of Cash”

Cashier’s checks often show up in used car purchases. It feels official: you walk into a bank, request a check payable to the seller, and leave with a bank-backed instrument.

People like the simplicityone check, one transaction. But there’s also a common “aha” moment: cashier’s checks still require smart logistics.

Buyers learn to confirm the seller’s exact legal name, coordinate meeting times around bank hours (because not every transaction happens at 2:00 p.m. on a Tuesday),

and keep the check secure until the handoff. It’s not complicated, but it’s not the kind of item you casually toss on your car seat next to an open coffee.

Experience #4: The Scam Story That Changes How People Receive Payments

On the receiving side, many “experiences” come from online marketplaces. Someone sells a laptop, a sofa, or a vehicle and a buyer insists on sending a cashier’s checksometimes for more than the item costs.

The buyer may sound polite, even professional. The check may look pristine. And then comes the line: “Can you send back the extra amount today?”

People who’ve been through (or narrowly avoided) this scam often become passionate about two rules:

(1) Never refund overpayments, and (2) Don’t treat a deposit as final just because your app shows it.

Banks can reverse funds if the instrument is counterfeit. That’s why cautious sellers insist on safer payment methods for marketplace deals

(or they only complete the sale at the issuing bank, where verification is more straightforward).

Experience #5: The “Why Did They Ask for My ID?” Surprise

For larger purchases of money orders or similar instruments, people are sometimes surprised when asked for ID.

The experience can feel annoyinguntil they understand it’s part of anti-fraud and anti–money laundering compliance.

The practical takeaway is simple: if you’re planning a larger purchase, bring identification and expect that the transaction may take longer than a coffee run.

These real-life lessons all point to the same conclusion:

money orders and cashier’s checks are excellent tools when used correctly, but the best results come from planning the detailslimits, payee names, receipts, verification, and timing.