Table of Contents >> Show >> Hide

- The reality check: medical school debt is commonand it’s often enormous

- What “desensitized to debt” really means in medical training

- Debt isn’t just “a number”: how it can shape decisions and well-being

- So… does med school “desensitize” doctors to debt? Often, yesbut not in the way people think

- The “debt infrastructure” that makes big balances feel manageable

- Why the debt talk in medicine can feel strangely casual

- What would help: reducing debt numbness without adding shame

- Final verdict: med school can desensitize doctors to debt, but it doesn’t make them immune

- Experiences that capture the “debt desensitization” journey (composite snapshots)

In most careers, six figures is a salary. In medical school, six figures is… Tuesday.

And if you’ve ever wondered whether med school “desensitizes” doctors to debt, you’re not alone.

The question pops up because the numbers are so big they start to feel less like money and more like weather:

“Yep, looks like a 30% chance of loan interest with scattered panic.”

But “desensitized” doesn’t mean “unbothered.” It usually means normalizedthe debt becomes part of the background noise of training,

like pager beeps, shelf exams, and that one attending who asks questions in the exact tone of a courtroom drama.

Let’s look at what the data says, what the culture feels like on the ground, and why a debt balance can become both

oddly invisible and painfully real at the same time.

The reality check: medical school debt is commonand it’s often enormous

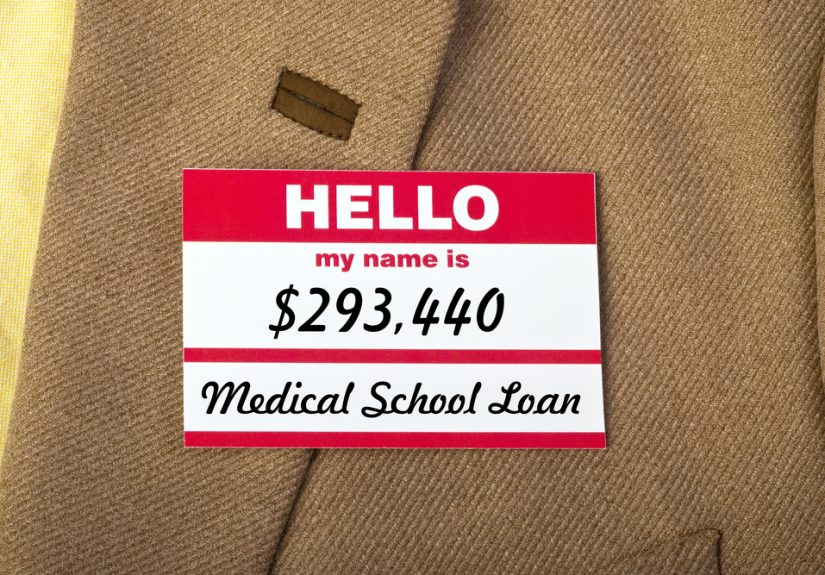

To understand the “debt numbness” phenomenon, start with the scale. National AAMC data for the Class of 2024 shows that

71% of graduates had education debt (including both undergraduate and medical school borrowing),

with a mean debt of $212,341 among those who borrowed. The median among borrowers was $205,000.

About 23% of graduates carried $300,000 or more in total education debt. And 63% said they planned to enter a loan

forgiveness or repayment program.

Those figures don’t land in a vacuum. The same AAMC snapshot lists a median four-year cost of attendance approaching

$286,454 at public schools and $390,848 at private schools (class of 2025, based on the 2023–24 cost structure).

Translation: before anyone earns attending-level money, they’ve often bought a very expensive ticket to the privilege of being

asked to “present the patient” while running on three hours of sleep.

It’s also not evenly distributed. AAMC’s school-level data shows wide variation in the percentage of students receiving aid and the

average graduate indebtedness by institution. Some programs have unusually low indebtedness (often due to major scholarship models),

while others show much higher average debt figures. That spread matters because “debt desensitization” tends to be strongest where

big balances are seen as routine, expected, and shared by nearly everyone in the cohort.

What “desensitized to debt” really means in medical training

Desensitization isn’t a moral failing. It’s a coping strategy the brain uses when confronted with a constant stressor.

If every day includes (1) a workload that could humble a robot and (2) a loan balance that could buy a small castle,

your mind will eventually try to file one of those into a folder labeled “Not Today.”

In med school, debt often shifts from being a shocking number to being an assumptionlike having to learn

the Krebs cycle, or that your “quick question” will take 45 minutes.

The result can look like desensitization, but it’s more like a three-part cocktail:

normalization, delayed consequences, and professional social proof.

1) Normalization: “Everyone has it, so it must be… fine?”

Humans take cues from their surroundings. When most of your peers are carrying similar balances, the debt stops feeling like a personal emergency

and starts feeling like an admissions requirement (right next to organic chemistry and emotional resilience).

Students swap loan totals the way other people swap gym routineshalf serious, half joking, and fully aware that it’s weird.

There’s also a practical side: many medical students don’t have time to obsess over finances. When your calendar is a game of Tetris

involving anatomy lab, clinical skills, research, and exams, “financial anxiety” can get downgraded to “later, maybe, after Step.”

It’s not denial as much as triage.

2) Delayed consequences: the debt feels abstract until repayment becomes real

Medical education debt often doesn’t demand immediate repayment in the same way rent does. Students can borrow, enroll, defer, repeat.

During residency, repayment may shift into income-driven plans or other structures, but the full weight of the balance can still feel distant

compared to today’s problemslike figuring out why the patient’s potassium is doing interpretive dance.

This delay is part of why debt can feel oddly unreal. People adapt to what they must solve today.

Debt becomes most emotionally “loud” at transition points: graduating, matching, moving, starting repayment, buying insurance, trying to rent

in a high-cost city on a resident stipend, or realizing your loan servicer emails you more often than your friends do.

3) Social proof and professional identity: “Doctors make good money, so it’ll work out”

Future income is the most common psychological anesthetic. The Bureau of Labor Statistics notes that physician and surgeon wages are

among the highest, with a median wage at or above $239,200 per year (category-level reporting varies by specialty).

That expectation encourages a mindset of “this is an investment.”

And it often isover a career, physician earnings can be substantial. But the path is long, and the timing matters.

A high future income doesn’t erase the reality that many trainees spend years earning far less than that while interest accrues,

life happens, and costs don’t politely wait their turn.

Debt isn’t just “a number”: how it can shape decisions and well-being

Here’s where the plot thickens. If doctors were truly “desensitized,” the debt would be emotionally irrelevant.

But research and on-the-ground reporting suggest a more complicated picture: debt may be normalized culturally while still influencing

stress, career thinking, and life choices.

Financial stress and wellness: the quiet contributor

Training is already intense, and financial strain can add friction. Some work has highlighted the link between financial stress and physician well-being,

suggesting money pressure can intersect with burnout and overall wellness.

Meanwhile, the AMA has reported national data showing resident burnout trends and variations by training year, illustrating that the resident experience

can be psychologically demanding even before finances are layered on top.

Debt also affects day-to-day choices in ways that don’t always show up in a spreadsheet:

delaying marriage or children, postponing home ownership, avoiding lower-paying geographic areas despite a desire to serve there,

or feeling trapped in a schedule that leaves little room for financial planning.

Even when someone is “used to” the debt, they may still feel boxed in by it.

Does debt influence specialty choice? The evidence is nuanced

The common belief is simple: more debt pushes students toward higher-paying specialties. But the research story is less tidy.

Older and newer studies have debated how much debt actually shifts specialty choice compared with factors like interest, lifestyle, mentorship,

and perceived fit.

For example, research in major medical journals has explored the relationship between medical student debt and career decisions over time,

with findings that don’t always align neatly with the “debt equals specialty” narrative.

Some studies have found limited association once other variables are considered, while others suggest debt may play a role in specific contexts

or at certain thresholds.

A fair summary is this: debt can be a factor, especially when paired with other pressures,

but it’s rarely the only driver. Medicine is a deeply identity-based career. Many students pick their specialty because they love the work,

not because their loan balance whispered, “Orthopedics…”

So… does med school “desensitize” doctors to debt? Often, yesbut not in the way people think

If we define desensitization as “less emotional reaction to a large number,” then yesmedical training often normalizes debt.

Students and residents commonly talk about debt as a constant companion rather than a daily crisis.

When borrowing is widespread (and the pathway to repayment is long), a certain numbness is almost inevitable.

But if we define desensitization as “debt has no effect,” then nobecause debt can still influence:

- Stress load: adding financial uncertainty to already demanding training.

- Life timing: delaying saving, family planning, and housing decisions.

- Career flexibility: limiting risk-taking (like starting a practice or choosing a lower-paying setting early on).

- Geography and service choices: nudging people away from areas with high costs or lower salaries.

In other words, many doctors become accustomed to the debt while still carrying its weight.

It’s like getting used to wearing a heavy backpack: you stop noticing it every minute, but it still changes how you move.

The “debt infrastructure” that makes big balances feel manageable

One reason debt can feel less terrifying in medicine is that there are established repayment pathwaysespecially for federal loans.

Medical trainees hear about these routes early, and that knowledge can reduce panic (or at least give the panic a PowerPoint slide).

Public Service Loan Forgiveness (PSLF)

PSLF is frequently discussed because many physicians work for nonprofit or public hospitals during training and beyond.

Federal Student Aid describes PSLF as forgiving the remaining balance on Direct Loans after a borrower makes

120 qualifying monthly payments under a qualifying repayment plan while working full time for a qualifying employer.

Because it requires 120 payments, it generally takes at least 10 years to qualify.

The key cultural effect: PSLF makes debt feel less like a life sentence and more like a long, bureaucratic scavenger hunt.

(“Congrats! You found all 120 payments. Please submit your forms… again.”)

Income-driven repayment (IDR) and “residency-friendly” payment structures

Income-driven plans are designed to base payments on income, which can matter when a resident salary is modest relative to the debt.

AAMC’s Class of 2024 fact card even includes sample repayment illustrations for federal Direct Loans, showing how payments may differ during residency

versus after training depending on the plan assumptions.

That kind of official modeling helps explain why many graduates report planning to enter repayment or forgiveness programs.

Important reality check: programs can reduce monthly payment pressure, but they don’t remove financial stress entirely.

Paperwork, recertification, plan rules, interest dynamics, and life changes can all turn “manageable” into “Wait, why did my payment change?”

Still, knowing there are pathways can make the debt feel less immediately catastrophicone ingredient in the “desensitization” recipe.

Why the debt talk in medicine can feel strangely casual

Medical culture prizes endurance. Students learn to function in high-stakes environments, absorb vast information, and keep going.

That same endurance mindset can spill into finances: “This is hard, but temporary” becomes “This is expensive, but temporary.”

(Spoiler: “temporary” can last a decade.)

There’s also an unspoken comparison game. In many social circles, talking about $200,000 of debt would trigger an intervention.

In medical school, it might trigger a nod and a joke about naming your loans so you can greet them politely each morning.

And yes, humor is part of it. People joke about debt because it’s safer than spiraling.

A laugh doesn’t cancel the interest, but it can keep you from personally identifying as a human amortization table.

What would help: reducing debt numbness without adding shame

If we want to answer the original question with something useful, we should ask a follow-up:

is desensitization helpful or harmful?

A little normalization can prevent paralysis. But too much numbness can delay planning, discourage early financial literacy,

and increase stress later when repayment becomes unavoidable.

The sweet spot is confidence without denialknowing the numbers, knowing the options, and building a plan that doesn’t depend on “future me will handle it.”

Better financial education (without turning med school into “Accounting: The Musical”)

Many students graduate knowing the differential diagnosis for chest pain but not the difference between interest capitalization and compounding.

Some organizations provide debt-management guidance for trainees, and more schools are integrating basic personal finance education.

The goal isn’t to make every student a financial wizardit’s to prevent avoidable mistakes and reduce anxiety through clarity.

Greater transparency around cost and repayment realities

Cost of attendance numbers are often published, but students benefit most when they can see how borrowing translates into real-world monthly payments

during residency and early attending years. AAMC’s fact-card style modeling is a step in that direction.

Clarity reduces shame, and reduced shame makes it easier to ask for help.

Support for trainees facing disproportionate burden

Debt is not equally distributed across backgrounds. Students with fewer family resources often borrow more and have less “cushion” for emergencies.

That can amplify stress during training. Recognizing those differencesand supporting students through scholarships, advising, and targeted resources

can reduce both financial strain and the need for “numbness” as a coping strategy.

Final verdict: med school can desensitize doctors to debt, but it doesn’t make them immune

Medical school often trains people to tolerate discomfort and delay gratification. Debt fits neatly into that mindset.

So yes, many doctors become less emotionally reactive to large balancesthey normalize them, postpone dealing with them, and lean on future income

or structured repayment paths to make the situation feel survivable.

Yet debt still matters. It can influence stress, flexibility, and life milestonessometimes loudly, sometimes in the background.

The healthiest outcome isn’t numbness; it’s financial awareness with a plan, plus systems that don’t require a decade of paperwork

to feel like adulthood is allowed to start.

Experiences that capture the “debt desensitization” journey (composite snapshots)

The stories below are compositesnot one specific person’s diarybased on common themes medical trainees describe in public discussions

and in research about stressors in training. Think of them as a documentary montage, minus the dramatic voiceover.

Snapshot #1: The first loan disbursement (M1)

The email arrives: “Funds have been disbursed.” It sounds celebratorylike confetti should shoot out of your laptop.

Instead, you stare at your account balance wondering why your brain is doing math in slow motion.

The number feels too big to be real, so you do what any rational future physician would do: you buy the required textbooks,

a stethoscope, and the cheapest coffee maker that still looks like it has a will to live.

You tell yourself it’s an investment, and you’re right. But you also learn your first financial coping skill:

when the number is terrifying, you shrink it into monthly survival tasks.

Snapshot #2: Clinical rotations and “future me” budgeting (M3)

During rotations, debt becomes oddly quiet. Not because it’s gone, but because your brain has bigger emergencieslike

presenting a patient while your pockets contain four pens, two alcohol swabs, and exactly zero confidence.

The loan balance exists in a parallel universe with your student ID badge.

When someone asks about finances, you answer like you’re discussing the weather: “Yeah, it’s high.”

You start to notice a group norm: nobody is shocked anymore. The shock got replaced by a new emotiondetermination

and a shared joke that your loans have their own ZIP code.

Snapshot #3: Match Day whiplash (M4)

You match. You celebrate. You cry. You text everyone. Then you google “resident salary in [city]” and immediately learn that

the cost of living does not care how many people you helped on rotations.

This is when debt stops being abstract and becomes logistical: moving costs, deposits, licensing fees, board fees,

the mysterious expense category known as “everything.”

You don’t feel numbyou feel busy. The numbness is actually a form of focus.

You can’t solve a 10-year financial plan while you’re trying to figure out where you’ll live in three weeks.

Snapshot #4: Residency math (PGY-1 to PGY-3)

Your days are long. Your learning curve is vertical. Your paycheck arrives and leaves like it’s late for another appointment.

Debt becomes a background app running quietly, occasionally sending a notification that makes your stomach drop.

Some months you feel calm because you’ve chosen a repayment strategy. Other months you feel annoyed because the rules are complicated.

The “desensitization” is inconsistentone minute you shrug, the next minute you’re calculating whether you can attend a wedding

without your budget filing a formal complaint.

Snapshot #5: The first attending paycheck (and the first reality check)

The paycheck finally looks like what people assume doctors earn. Friends say, “Now you’re set!”

You smile, because you’re happybut you also know the fine print. Taxes exist. Retirement saving exists. Malpractice exists.

And that loan balance still exists, waiting politely like a bouncer outside adulthood: “Name on the list?”

The debt doesn’t vanish overnight. But something changes: for the first time, you can see the finish line.

The goal isn’t to stay numb. The goal is to stay steadyaware enough to plan, calm enough to live your life anyway.