Table of Contents >> Show >> Hide

- The Easiest Way to “Win” a Market Argument

- Value Isn’t Dead. It’s Just… Dramatically Resting

- The Small-Cap Value Plot Twist

- When “Left for Dead” Starts Running Again

- The Nasdaq 100: “Wait… Only 8%?”

- Gold: The Chart That Annoys Stock People

- The Rest of the World: “Excuse Me, We’re Still Here”

- The “Boring” Charts That Save Real Portfolios

- So… What Should You Do With All This?

- Experience Notes: What These Charts Feel Like in Real Life (500+ Words)

Charts are the closest thing finance has to a magic trick. One minute you’re looking at “proof” that something is

obviously true, and the next minute you change the time period andpoofyour “proof” turns into a pumpkin.

That’s not because charts are evil (although some of them definitely have villain energy). It’s because markets are messy,

cyclical, and allergic to neat narratives. The bigger the story“tech always wins,” “value is dead,” “gold is useless,”

“international stocks are a charity project”the more likely a chart exists somewhere that will dunk on it.

This post is a tour of surprising charts and what they’re really trying to tell you: not “buy this now,” but

“be careful what you believe,” “watch your assumptions,” and “maybe don’t build a retirement plan on a three-year hot streak.”

The Easiest Way to “Win” a Market Argument

Want to win any investing argument at a dinner party? Don’t bring a better argument. Bring a better start date.

Start at the top of a bubble and the chart screams “stocks are a scam.” Start at the bottom of a crash and the chart

screams “anyone who didn’t buy that dip hates money.”

Markets don’t move in straight linesthey move in chapters. If you only show one chapter, you can make the hero look like a villain

or the villain look like a misunderstood poet with a tragic backstory.

Why this matters in real life

The biggest investing mistakes usually aren’t math mistakes. They’re narrative mistakes:

“This has worked for years, so it will keep working,” or “That was terrible, so it will always be terrible.”

Charts can either reinforce those stories or rescue you from themdepending on whether you zoom in or zoom out.

Value Isn’t Dead. It’s Just… Dramatically Resting

Every few years someone announces, with the confidence of a weather app that’s never been wrong (so, never),

that value investing is finished. The logic is always the same: growth is winning, tech is dominant, the old rules are obsolete,

and value investors should pack up their calculators and take up pottery.

But the longer you study markets, the more you notice a pattern: styles don’t “die.”

They rotate, sometimes painfully, and often at the exact moment the crowd has decided the rotation will never happen again.

What the “value is dead” chart usually hides

- Valuation starting points. Paying more for a dollar of earnings can work for a long timeuntil it doesn’t.

- Interest-rate and inflation regimes. Different backdrops can tilt the advantage between long-duration growth and cash-flow-heavy value.

- Concentration. When a handful of mega-winners dominate, style performance can look like destiny instead of a cycle.

The takeaway isn’t “value will beat growth next week.” It’s “style leadership changes, and pretending otherwise is how investors end up

chasing yesterday’s winners at tomorrow’s prices.”

The Small-Cap Value Plot Twist

Here’s a surprise that makes people blink twice: small-cap valueboth U.S. and internationalhas outperformed over a recent five-year window,

even after years of being treated like the investing equivalent of a flip phone.

International small-cap value, in particular, tends to shock people because the popular narrative has been:

“U.S. big tech is the only game in town.” When a chart shows the “boring stuff” winning for a meaningful stretch, it forces a hard question:

were you investing, or were you just shopping for the best recent chart?

Why small caps can surprise

Small caps aren’t just “mini large caps.” They’re exposed to different economic forces:

domestic revenue, credit conditions, and shifts in business cycles can matter more. They can also benefit when leadership broadens beyond the

same handful of giants that have been carrying the headline indexes.

The honest message from this chart is not “small caps are back forever.”

It’s: the market loves embarrassing certainty. The minute an asset class is declared uninvestable, it becomes a candidate for a comeback.

When “Left for Dead” Starts Running Again

Another chart twist comes from short, punchy windows around sell-offs and rebounds. Coming off a market drop, performance leadership can flip fast:

small caps can lead, mid caps can keep up, and the giants can take a breather without “breaking” the whole market.

One reason investors miss these shifts is psychological: if something has disappointed you for years, you stop looking.

That’s when the turning points sneak inquietly, without a press conference.

A practical implication: don’t confuse “recently painful” with “permanently broken”

If your portfolio only owns what has been working lately, you’re not diversifiedyou’re just late.

Diversification is owning things that take turns being annoying.

The Nasdaq 100: “Wait… Only 8%?”

Here’s a chart that messes with your memory: the Nasdaq 100 compounding at roughly 8% per year since 2000.

That sounds impossible if you’ve lived through the post-2013 rocket ship phase, when tech-heavy indexes delivered monster returns.

The explanation is brutally simple: sequence matters. A huge loss early on can drag a long-term average down for years,

even if a huge boom arrives later to rescue the headline number.

The lost decade effect (and why your brain hates it)

From 2000 through 2012, the Nasdaq 100’s total return was negative overall, and the drawdown after the dot-com peak was catastrophic.

Combine a massive bear market with a massive bull market and you can end up with results that feel… oddly ordinary.

This is why “the market always goes up” is both true and misleading. It goes up eventually.

The problem is that “eventually” can be a long time when you’re living inside the chart instead of reading about it later.

What this teaches

- Recency bias is expensive. The best recent performer can have the worst future decade.

- Concentration risk is real. A narrow leadership era can inflate confidence right before the music changes.

- Patience isn’t passive. Holding through ugly stretches is an active decision with emotional costs.

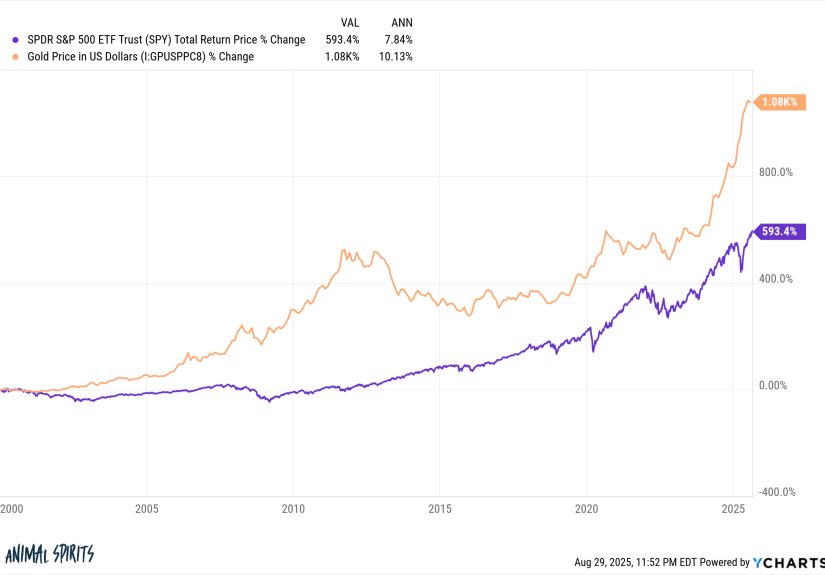

Gold: The Chart That Annoys Stock People

Another chart surprise: gold outperforming the S&P 500 over the stretch starting around 2000. If your mental model is

“gold is a shiny pet rock,” that chart feels like a personal attack.

But once again, starting points matter. Gold entered that period after a long bear market. U.S. stocks entered after a long bull run.

The early 2000s also delivered exactly the kinds of environments where gold tends to look better than usual: market stress, policy shifts,

inflation scares, and real-rate whiplash.

What the gold chart really says

It does not say, “sell everything and buy bars.” It says:

- Different assets shine in different decades. Even the “obvious winner” can get humbled.

- Non-income assets can still matter. Gold doesn’t pay dividends, but it can diversify certain risks.

- Timing dominates short narratives. If you start at extremes, you can make almost anything look inevitable.

The Rest of the World: “Excuse Me, We’re Still Here”

Many U.S. investors treat international stocks like the side salad they didn’t order. Then a year shows up where

non-U.S. markets outperform, and suddenly everyone remembers there are other countries with companies that sell things people want.

A broad “international beats U.S.” year can feel shocking mainly because of home-country biasthe habit of assuming your

domestic market is the only market that counts. It’s comfortable, familiar, and reinforced by headlines that treat the S&P 500 like

“the stock market” instead of “one stock market.”

Why this chart matters even if you love U.S. stocks

- Leadership rotates globally too. The U.S. has long stretches of dominanceand long stretches of catching its breath.

- Currency and valuation differences are real. They can help or hurt, but they diversify the drivers of return.

- Global diversification can reduce single-country regret. You’ll still have regret. Just not all from the same place.

The “Boring” Charts That Save Real Portfolios

The surprising charts are fun. The boring charts are what keep you from doing something regrettable at 2:00 a.m.

Let’s connect the dots into a few principles you can actually use.

1) Volatility is the admission price

Stocks frequently suffer meaningful pullbacks within a calendar year, even in years that finish positive.

If your plan assumes “no scary dips,” your plan is not a planit’s a wish.

2) Missing the best days can wreck long-term results

The stock market’s strongest up days tend to cluster around the worst down days. That’s why market timing is so punishing:

you don’t just have to be right onceyou have to be right twice (when to get out and when to get back in),

often during the most emotionally chaotic moments.

3) Investors often earn less than their investments

One of the crueler “charts” is the gap between what funds earn and what investors actually take home.

When people chase performance, panic-sell, and then buy back after a rebound, the market isn’t stealing from them.

They’re accidentally tipping the market.

4) Diversification isn’t about maximizing returns every year

Diversification is a behavioral tool as much as a math tool. It helps you stick with a strategy by ensuring

you’re never 100% dependent on one story being true.

A simple framework that respects these charts

- Pick a mix you can hold through a bad year without self-sabotage.

- Automate contributions so your plan doesn’t require daily courage.

- Rebalance on a schedule (not a feeling) to buy what’s lagging and trim what’s frothy.

- Measure success by goal progress, not by beating your neighbor’s favorite ETF.

So… What Should You Do With All This?

The point of “surprising charts” isn’t to make you cynical. It’s to make you humble in the best way:

humble about forecasting, humble about narratives, and humble about how hard it is to behave well when your portfolio is

impersonating a roller coaster.

If you want a one-sentence summary, it’s this: build a portfolio that doesn’t require you to be a prophet.

Because the market has a long history of making prophets look like comediansand not the funny kind.

Experience Notes: What These Charts Feel Like in Real Life (500+ Words)

Charts are tidy. Real investing is not. In the real world, nobody sits in a quiet room with a cup of tea saying,

“Ah yes, a perfectly normal 14% intra-year drawdown, as expected.” In the real world, a 14% drop feels like the universe

personally chose your portfolio as the designated stress test.

One common “experience moment” looks like this: an investor finally commits to a plan after watching a hot sector soar.

They buy it because it feels safeeveryone they follow loves it, the headlines praise it, and the chart is basically a staircase.

Then the sector flatlines or dips. Nothing catastrophic. Just enough boredom and regret to make the investor wonder if they made a mistake.

That’s when a different chart starts seducing them: the new hot thing. And suddenly the portfolio becomes a revolving door of

“things that just stopped working,” which is a painful way to recreate the investor return gap.

Another experience moment happens when value or small caps start doing well after being ignored for years. The first reaction isn’t joy.

It’s suspicion. People don’t trust a comeback at first. They assume it’s a fake rally or a trap because their last memory of that asset class

is disappointment. That’s the emotional reason diversification works: you keep a slice of the market’s “unpopular areas” in your portfolio

so you’re already on the train when it starts movingrather than sprinting after it once the headlines notice.

The Nasdaq “only 8% since 2000” idea is a perfect example of how lived experience differs from the neat long-term average.

If you invested near a peak and endured a brutal drawdown, the eventual recovery doesn’t feel like victoryit feels like survival.

You didn’t experience a smooth 8% line; you experienced a decade where hope had to be renewed monthly.

Then, if you held on long enough to reach the booming years, you probably felt vindicated… right until you saw that the long-term

average can still look ordinary when you include the ugly chapter. That’s a humbling lesson about sequence-of-returns risk and why

“great long-term returns” can still be emotionally hard to earn.

Gold charts create a different kind of real-world tension. People rarely buy gold because they’re thrilled.

They buy it because they’re uneasy about somethingpolicy, inflation, currency, geopolitics, the vibe of the world.

When gold underperforms stocks for years, it’s easy to call it pointless. When gold outperforms during scary stretches, it suddenly feels

“smart,” even if you bought it for the wrong reason or at the wrong time. The experience lesson is that every diversifier looks dumb

right up until the moment you’re grateful it exists.

The most practical experience lesson from all these charts is behavioral: the goal is not to build a portfolio that never surprises you.

That portfolio doesn’t exist. The goal is to build a portfolio whose surprises don’t cause you to panic, abandon your plan,

or chase a new story at the worst possible time. If your strategy depends on perfect timing, constant certainty, or flawless discipline,

it’s not a strategyit’s a fantasy with a brokerage account.

So when you see a surprising chart, don’t treat it like a trading signal. Treat it like a mirror. Ask:

“Which story am I believing too strongly?” and “What would I do if the next decade looks nothing like the last five years?”

That’s the wealth-of-common-sense version of investing: fewer predictions, better habits, and a portfolio built to survive reality.