Table of Contents >> Show >> Hide

- What “Don’t Fight the Fed” Really Means

- Where the Phrase Came From (And Why It Stuck)

- When “Don’t Fight the Fed” Works Best

- When the Mantra Fails (Or Gets People Into Trouble)

- A Practical Way to Use the Idea (Without Turning It Into a Meme)

- Specific Examples Investors Often Point To

- Common Myths (And the Reality Check)

- So… Should You “Remember Don’t Fight the Fed” Today?

- Experiences That Bring the Mantra to Life (A 500-Word Reality Tour)

There’s an old market saying that gets repeated whenever stock prices start wobbling and a Federal Reserve official clears their

throat at a microphone: “Don’t fight the Fed.” It’s the investing equivalent of “don’t argue with someone holding the

remote”except the remote controls interest rates, liquidity, and the collective mood of Wall Street.

But here’s the twist: people often quote the phrase like it’s a magic spell. Say it three times, throw a chart at the wall, and

boomyour portfolio is protected. In real life, “don’t fight the Fed” is less of a fortune cookie and more of a framework:

the Fed shapes financial conditions, and financial conditions shape markets. The trick is knowing what the Fed is actually doing,

what the market already expects, and when the slogan stops being useful.

What “Don’t Fight the Fed” Really Means

At its core, the mantra is about monetary policyhow the Federal Reserve influences borrowing costs and credit conditions

to pursue its economic goals. When money is cheaper and easier to get, businesses and consumers tend to spend more, profits can look

better, and investors often feel bolder. When money is expensive and harder to get, the opposite can happen: growth slows, risk-taking

cools, and markets can get jumpy.

The Fed’s Big Levers: Rates, Expectations, and “Financial Conditions”

The Fed’s best-known lever is the federal funds ratean overnight rate in the banking system that influences a whole chain

of other rates (credit cards, mortgages, business loans, bond yields). When the Fed raises or lowers its target range, it’s trying to

push the economy toward its mandate: maximum employment and stable prices (you’ll often hear this called the “dual mandate”).

But the Fed doesn’t just move rates; it also moves expectations. If investors believe the Fed will cut rates later, long-term

yields may fall today. If investors think the Fed will stay restrictive, markets can tighten before the next meeting even happens.

That’s why press conferences and policy statements can swing markets like a door in a hurricane.

This all rolls into a bigger concept: financial conditions. Think of financial conditions as the “weather” for investing:

interest rates, credit spreads, stock valuations, bank lending, and overall ease of getting money. When conditions are “loose,” risk assets

(like stocks) often find it easier to rally. When conditions are “tight,” markets usually have a tougher time sprinting uphill.

Why Rates Hit Stocks: The Discount-Rate “Gravity” Effect

Stocks represent future cash flows. A simple way to think about valuation is: the more you have to “discount” future earnings back to today,

the less those future dollars are worth now. When interest rates rise, the discount rate often rises tooso the same expected earnings can

justify a lower stock price.

This doesn’t mean every rate hike instantly crashes the market. It means higher rates act like gravity:

they make it harder for valuations to float at the same altitude. That’s especially true for long-duration assetscompanies whose

profits are expected far in the future (often growth and tech stocks). Meanwhile, some sectors can behave differently: banks may earn more on

lending spreads, and some value/cyclical areas can benefit if the economy stays sturdy.

Where the Phrase Came From (And Why It Stuck)

The saying is widely associated with investor and market commentator Marty Zweig, who popularized the idea that fighting the Fed’s

policy stance is a bad bet over time. The reason it stuck is pretty simple: it gives investors a north star in the chaos.

Markets are loud, emotional, and frequently convinced that “this time is different.” The Fed, for better or worse, is one of the few actors that

can change the cost of money for the entire economy.

Over decades, the market has repeatedly rediscovered the same lesson: if the Fed is aggressively tightening to cool inflation, financial conditions

often worsen and risk assets can struggle. If the Fed is easing to support growth or stabilize the system, conditions often improve and risk appetite

can return. That’s the logic behind the mantra.

When “Don’t Fight the Fed” Works Best

The slogan tends to be most useful in big, obvious policy regimeswhen the Fed is clearly easing or clearly tightening, and the market

hasn’t fully priced it in yet.

1) The Fed Is Easing, Liquidity Improves, and Risk Appetite Grows

In easing regimes, borrowing costs can fall, refinancing becomes easier, and investors often shift from “protect the principal” to “chase returns.”

Stocks don’t rise just because rates fallbut lower rates can support higher valuations and reduce pressure on leveraged balance sheets.

Historically, many investors watch the start of a rate-cut cycle as a signal that the policy headwind may become a tailwind. It’s not a guarantee

the economy mattersbut it can be a meaningful shift in the market’s backdrop.

2) The Fed Signals It Will Stay Supportive

Guidance matters because markets are forward-looking. Sometimes the Fed can loosen conditions without immediately cutting rates, simply by convincing

markets that it will act if needed. This is one reason investors track the Fed’s communications so intensely:

the message can move yields and risk sentiment almost as much as the decision itself.

When the Mantra Fails (Or Gets People Into Trouble)

“Don’t fight the Fed” can fail for a few reasonsusually because the phrase is being used as a shortcut instead of a tool.

1) The Market Moves Before the Fed

If everyone expects the Fed to cut rates six months from now, markets may rally long before the first cut. By the time the cut arrives, it can be

“old news,” and prices may respond lessor even fall if investors worry the cut is happening for a bad reason (like a weakening economy).

2) The Fed Cuts Because Something Broke

This is the classic plot twist. Investors cheer “rate cuts!” but the reason matters. If cuts are a response to recession risk or financial stress,

corporate earnings can drop and stock prices can struggle even with lower rates. In other words:

the Fed can be supportive and the market can still be unhappybecause the economy is writing the main storyline.

3) Inflation Changes the Rules of the Game

When inflation is high, the Fed may keep policy restrictive longer than markets want. In that environment, wishful thinking can become an expensive

hobby. Investors who ignore inflation trends can end up positioned for “easy money” that never arrivesor arrives later, after the market has already

repriced risk.

A Practical Way to Use the Idea (Without Turning It Into a Meme)

If you want a usable version of “don’t fight the Fed,” treat it like a three-part checklist:

(1) What is the Fed trying to do? (2) What does the market already expect? (3) What does that mean for financial conditions and earnings?

Step 1: Identify the Fed’s Mission in This Moment

The Fed’s job is not “make the S&P 500 happy.” Its mandate is about employment and price stability. When inflation is stubborn, policy may stay tighter.

When the labor market weakens meaningfully, the Fed may shift toward support. The key is to connect the Fed’s actions to its goalsnot to your watchlist.

Step 2: Watch the “Expected Path,” Not Just the Current Rate

Markets care about where rates are going, not just where they are. That’s why investors pay attention to:

- Fed communications (statements, press conferences, speeches)

- Economic projections and the broader message about risks

- Market pricing (what traders collectively imply about future policy)

A useful mental model: if the Fed does exactly what everyone expects, the market response may be muted. Big moves often happen when the Fed surprises

expectationsor when investors realize the economy is changing faster than the Fed.

Step 3: Track Financial Conditions Like You Track the Weather

Even if you don’t use complex models, you can watch a few “common sense” signals:

- Bond yields (especially longer-term Treasury yields) rising or falling

- Credit spreads widening (stress) or tightening (confidence)

- Equity valuations expanding or compressing

- Dollar strength and global liquidity cues

When conditions are tightening fast, speculative assets often suffer first. When conditions are easing, breadth can improve and more parts of the market

participate. Think of it as the difference between skating on fresh ice versus skating on a puddle that looks frozen.

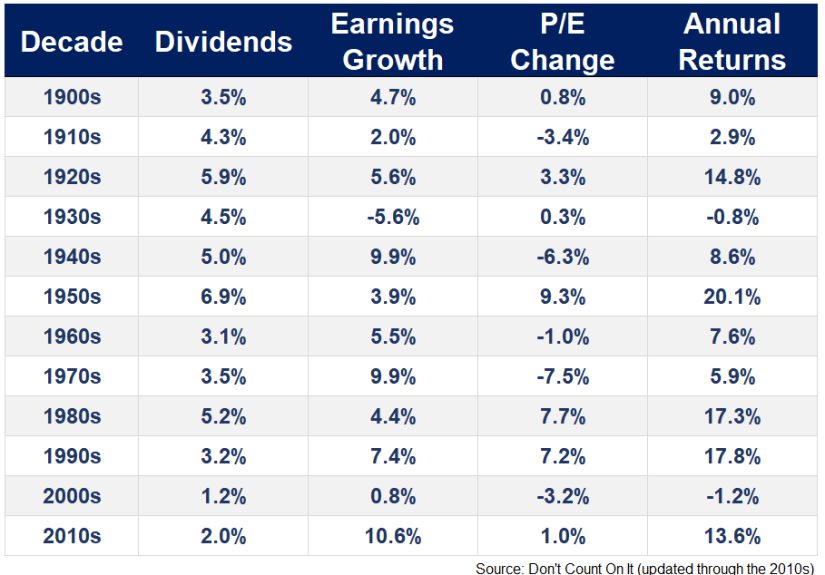

Specific Examples Investors Often Point To

Without turning history into a highlight reel (because markets love to ruin simple stories), here are patterns investors often cite:

Easing After Stress: The “Support Arrives” Pattern

During periods of financial stress, the Fed has sometimes eased policy and used other tools to stabilize markets and the economy.

When conditions improve, risk assets can recoversometimes dramatically. But the timing can be messy, because the economy may still be healing while

investors are already looking ahead.

Tightening to Fight Inflation: The “Valuations Come Back to Earth” Pattern

When inflation rises and the Fed tightens, valuations can compress, especially in areas priced for perfection. Companies with real earnings power can

still perform, but “hope stocks” (the ones living on future dreams) may have a harder time convincing investors to pay tomorrow’s price today.

Common Myths (And the Reality Check)

Myth: “If the Fed hikes, stocks must fall.”

Reality: Stocks can rise during hiking cycles if earnings growth is strong, if hikes are gradual, or if markets were braced for worse.

Policy is a major forcebut it’s not the only force.

Myth: “Rate cuts guarantee a bull market.”

Reality: Cuts can coincide with recessions. Lower rates may help later, but they don’t instantly repair earnings or confidence.

Myth: “The Fed controls the stock market.”

Reality: The Fed influences the cost of money and financial conditions. Markets still react to profits, productivity, geopolitics, innovation, and

occasionallyplain old investor mood swings.

So… Should You “Remember Don’t Fight the Fed” Today?

Remember it the way you remember a seatbelt: not because it guarantees you’ll never hit a pothole, but because it improves your odds when the road gets rough.

The most useful version of the mantra is:

align your risk-taking with the direction of policy and financial conditionswhile still respecting earnings and the economy.

If the Fed is tightening and inflation risks are high, assume the market will be more sensitive, valuations less forgiving, and “story stocks” more fragile.

If the Fed is easing and conditions are loosening, assume risk appetite can expandbut stay alert to why easing is happening.

Educational note: This article is for informational purposes and isn’t personalized investment advice. Your goals, timeline, and risk tolerance matter.

Experiences That Bring the Mantra to Life (A 500-Word Reality Tour)

Investors don’t really learn “don’t fight the Fed” from a textbook. They learn it from the moment their confidence meets a rate surprise.

One common experience is the “I thought the headline was bullish” whiplash: a new investor sees inflation cooling, assumes rate cuts are imminent,

buys high-growth stocks, and then watches the market drop because the Fed signals it still isn’t comfortable. The lesson isn’t that the investor was foolish;

it’s that markets trade on expectations versus reality. If everyone already expected good news, good news can feel disappointingly normal.

Another classic experience comes from long-term investors who lived through periods when bonds finally started paying “real money” again.

When yields rise, some people notice something odd: their diversified portfolio behaves differently. Stocks wobble, bonds drop (because bond prices fall

when yields rise), and suddenly the usual “stocks down, bonds up” comfort blanket doesn’t feel as cozy. That experience often leads to a deeper understanding

of policy regimes. In a low-rate era, duration risk can hide in plain sight. In a rising-rate era, it shows up like an uninvited guest who eats all the chips.

There’s also the “business owner lens.” Entrepreneurs and small-business operators often feel Fed policy before investors do: higher rates can raise the cost of

inventory financing, lines of credit, or expansion plans. One owner might delay hiring because debt service is higher; another might raise prices to protect margins.

When enough businesses make those decisions at once, growth can slow, and the market’s narrative shifts from “soft landing” optimism to “earnings risk” caution.

People who invest while also running a business often describe this as the moment the Fed stops being a TV topic and becomes a monthly expense line item.

Finally, many investors have lived through a humbling version of the mantra: the Fed can be “right” about inflation risks and the market can still rally for a while.

That creates temptation to ignore policyuntil conditions tighten enough that weaker balance sheets start cracking. The experience is usually gradual, not dramatic:

credit gets a little pricier, refinancing windows narrow, and investors become picky about profitability. The big realization tends to be this:

you can argue with the Fed, but you still have to pay the interest rate.

The most seasoned takeaway from these experiences isn’t blind obedience to policy; it’s disciplined humility. You don’t have to worship the Fed.

You just have to respect what changes when the price of money changesbecause almost everything eventually does.