Table of Contents >> Show >> Hide

- Why This Question Matters Right Now

- What “Simpler” Should Mean in Pension Investing

- The Bull Case for a Simpler CalPERS Model

- The Bear Case: Where “Simpler” Can Go Wrong

- What the Broader U.S. Evidence Suggests

- A Practical Framework for CalPERS: Simple Core, Sophisticated Edges

- Core Principle 1: Keep the total-fund benchmark brutally clear

- Core Principle 2: Build an explicit “complexity budget”

- Core Principle 3: Expand internal capabilities where scale supports it

- Core Principle 4: Separate policy clarity from tactical flexibility

- Core Principle 5: Measure success over full cycles, not one headline year

- How to Tell If the Simpler Approach Is Actually Working (2026–2028 Checklist)

- What This Means for Members, Employers, and Taxpayers

- Conclusion: Does CalPERS Need a Simpler Approach?

- Extended Experience Section (About ): What This Looks Like in Real Life

If you’ve ever opened a public pension investment report and immediately needed a snack break, you’re not alone.

Public pension portfolios can look like a spaceship control panel: private equity sleeves, credit buckets, inflation overlays,

real assets, internal/external management splits, benchmark layers, and about eleven acronyms per paragraph.

So when CalPERSthe largest public pension fund in the United Statesmoves toward a total portfolio approach and a cleaner reference benchmark, the obvious question is:

Does CalPERS need a simpler approach?

Short answer: yes, but not “simple” as in simplistic. The real goal is decision clarity, cost discipline, and faster execution without sacrificing diversification, governance, or long-term return potential.

In other words, less spaghetti diagram, more flight dashboard.

Why This Question Matters Right Now

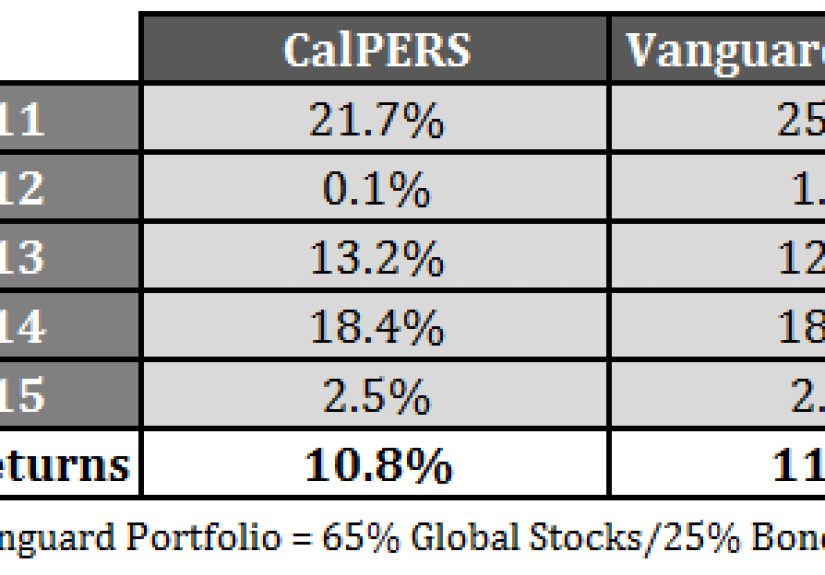

CalPERS has meaningful momentum: a strong recent one-year gain, improved funded status, and a governance shift that replaces multiple asset-class targets with a total-fund lens.

At the same time, the system still carries long-term obligations across millions of members and retirees. That means every strategic choice reverberates through three groups at once:

retirees who need benefit security, employers who face contribution volatility, and taxpayers who ultimately absorb policy mistakes.

The timing also matters. Across U.S. public pensions, funding improved from post-crisis lows, but the national picture is still mixed:

plans are better than they were a decade ago, yet not comfortably “mission accomplished.”

Translation: strong years help, but structure and discipline determine whether good years stick.

What “Simpler” Should Mean in Pension Investing

In pension strategy, “simple” should never mean “one-size-fits-all.” It should mean:

- Fewer moving parts in governance: fewer contradictory mandates and cleaner accountability.

- Clear benchmark architecture: one core reference portfolio plus explicit risk budget.

- Transparent cost stack: management fees, carry, consultants, overlays, and transaction costs visible in one place.

- Faster rebalancing and capital allocation: less committee lag, fewer policy bottlenecks.

- Decision rules before market stress: so no one improvises under pressure.

Real simplicity is about reducing organizational friction. It’s less “dumbing down” and more “don’t trip over your own process.”

The Bull Case for a Simpler CalPERS Model

1) One portfolio lens can improve investment decisions

Under traditional strategic asset allocation (SAA), each asset class can become a silo with its own mini-scoreboard.

That can unintentionally reward local wins that hurt total-fund outcomes. A total portfolio approach (TPA) flips that logic:

the question becomes, “Does this decision improve the whole fund on a risk-adjusted basis?”

This is especially useful in volatile environments. If spreads blow out or equity risk premia change quickly, staff can reweight exposures without waiting for a full policy rewrite.

In plain English: more steering, less anchoring.

2) A cleaner benchmark improves transparency

A single reference portfolio (rather than a long menu of asset-class benchmarks) makes it easier for board members, employers, journalists, and beneficiaries to judge whether active decisions are adding value.

If total fund return beats the reference after costs, skill is showing up. If not, complexity may be hiding underperformance.

For a fund of CalPERS’ size, that clarity is not cosmetic. It affects manager selection, risk discussions, public accountability, and policy trust.

3) Simpler structure can reduce expensive complexity

Large pension funds often pay for complexity in ways that don’t appear on page one:

external management fees, carried interest, performance fee asymmetry, legal structures, and implementation drag.

A simpler core architecture can expose which complexity is genuinely productive and which is just expensive theater.

Think of it this way: complexity should have to earn its rent. If a strategy adds 120 basis points gross but consumes 110 basis points in all-in costs and governance bandwidth,

it may be “sophisticated” but not useful.

The Bear Case: Where “Simpler” Can Go Wrong

1) Private markets still matter for mega-funds

CalPERS is not a small endowment with one CIO and three interns and a heroic spreadsheet.

It is a giant, long-horizon institution with real liabilities and a broad opportunity set.

Private equity, private credit, infrastructure, and real assets can still add diversification and return potential if execution is disciplined.

Over-simplifying into mostly public beta could reduce optionality.

2) One benchmark can hide concentration risk

A reference portfolio is useful, but it can also mask exposure concentration if oversight gets lazy.

“Single benchmark” should mean clear anchor, not “ignore sub-portfolio risk.” Governance still needs deep drill-downs:

liquidity stress testing, vintage risk, factor crowding, valuation lags, and downside scenario analysis.

3) Governance simplicity does not remove political reality

Public pensions operate in a political ecosystem: board elections, employer budgets, labor concerns, media narratives, and legal constraints.

Even the best investment model can underperform if governance incentives are noisy.

You can simplify the model; you can’t fully simplify democracy.

What the Broader U.S. Evidence Suggests

The cross-institution evidence is nuanced:

- Public pension systems rely heavily on investment earnings over the long run, so strategic design matters enormously.

- Assumed return trends have come down over time, reflecting more conservative long-term expectations.

- Some research suggests alternative asset complexity has not always translated into superior after-fee outcomes across all periods.

- Funding has improved in recent years, but most systems remain below fully funded levels and still sensitive to market shocks.

Put differently: neither extreme wins by default. “All complexity is bad” is wrong. “More complexity always adds alpha” is also wrong.

The winning formula tends to be simple core + selective complexity + strong internal governance.

A Practical Framework for CalPERS: Simple Core, Sophisticated Edges

Core Principle 1: Keep the total-fund benchmark brutally clear

Use the reference portfolio as the primary accountability anchor.

Report excess return versus the reference after all costs, and do it consistently.

If a strategy can’t explain its contribution to total-fund risk/return in plain language, that strategy should be on probation.

Core Principle 2: Build an explicit “complexity budget”

Every non-plain-vanilla strategy should carry a documented complexity budget:

governance hours, legal complexity, liquidity lockup, fee drag, valuation uncertainty, and operational burden.

Complexity is allowedbut it must be priced, tracked, and justified.

Core Principle 3: Expand internal capabilities where scale supports it

Internal management and co-investment can reduce fee leakage over time, especially for a fund this large.

This requires investment in staff quality, compensation design, and data systemsnone of which are cheap upfront.

But cost discipline over decades is a compounding advantage.

Core Principle 4: Separate policy clarity from tactical flexibility

Board sets risk guardrails, liquidity boundaries, and long-term objectives.

Staff executes tactically within those limits.

This reduces policy churn while allowing quick action in changing markets.

It also makes post-mortems more honest: was it a policy miss, or an execution miss?

Core Principle 5: Measure success over full cycles, not one headline year

One-year returns are attention-grabbing, not definitive.

Evaluation should prioritize rolling 5-, 10-, and 15-year outcomes, net of costs, versus reference portfolio and liabilities.

If simplification works, it should appear as:

steadier funding progress, lower cost drag, and fewer forced strategic pivots during stress.

How to Tell If the Simpler Approach Is Actually Working (2026–2028 Checklist)

If CalPERS wants to prove the new model works, stakeholders should monitor five concrete indicators:

- Net value-added vs. reference portfolio: persistent positive excess return after all fees and implementation costs.

- Funding trajectory quality: steady funded-ratio improvement without relying on unusually optimistic assumptions.

- Contribution stability: fewer painful jumps in required employer contributions.

- Liquidity resilience: no forced selling during volatility spikes, with clear stress-test disclosures.

- Cost transparency: annual reporting that shows total investment costs in a way non-specialists can understand.

If these five move in the right direction, simplification is not just a sloganit is a measurable upgrade.

What This Means for Members, Employers, and Taxpayers

For members and retirees

The priority is benefit security. A simpler, more accountable investment process can lower the odds of strategy whiplash and increase confidence that promises are funded over time.

For employers

Contribution rates are budget reality, not theory. Smoother funding progress helps cities, counties, and state agencies plan better, avoiding budget surprises that crowd out payroll, public safety, and services.

For taxpayers

Taxpayers do not get excited about benchmark architecture, but they do care about fiscal stability.

Better governance and clearer investment accountability reduce the probability of future emergency fixes.

Less drama, more predictability.

Conclusion: Does CalPERS Need a Simpler Approach?

YesCalPERS needs a simpler approach, but not a simplistic one.

The right model is clarity at the center, sophistication at the edges.

Keep the reference framework clean, allow tactical flexibility, demand evidence that complexity adds net value, and report results in language normal humans can read before coffee.

The move toward a total portfolio approach is directionally smart because it aligns governance with how risk actually behavesin one portfolio, not eleven disconnected scorecards.

But execution will determine whether this is a durable improvement or just a new label on old habits.

If CalPERS can pair simplified decision architecture with rigorous cost discipline and transparent reporting, it can improve funded status while reducing contribution pressure.

That’s not just good investing. That’s better public stewardship.

Extended Experience Section (About ): What This Looks Like in Real Life

In practical pension work, “simplicity” is less a theory and more an operating experience.

Across board meetings, employer finance offices, beneficiary town halls, and investment committee reviews, the same pattern appears:

when the framework is too complex, the organization reacts slower, explains less, and pays more.

When the framework is coherent, decisions become faster and accountability becomes obvious.

One recurring experience comes from employer budget teams.

They don’t sit around debating tracking error versus multi-factor covariance assumptions.

They look at contribution notices and ask, “Can we afford this without cutting services?”

When strategy complexity creates volatile contribution outcomes, budget officers feel it immediately.

They postpone hiring, defer maintenance, and patch over shortfalls with one-time fixes.

In those environments, investment jargon turns into public-service tradeoffs within months.

A simpler decision architecture does not remove all volatility, but it reduces avoidable surprises and improves planning confidence.

Another lived reality appears in board governance.

Trustees often receive huge packets, dense analytics, and competing expert views.

If the policy framework is fragmented, meetings drift into technical rabbit holes while the central question“Are we improving total-fund resilience net of costs?”gets diluted.

In stronger governance periods, trustees return repeatedly to a small set of anchor metrics:

funded progress, net value-added, cost efficiency, liquidity, and long-horizon risk.

That rhythm creates better oversight culture.

People disagree less about vocabulary and more about evidence, which is exactly where healthy disagreement belongs.

Investment staff experience this shift too.

In siloed models, teams can become asset-class defenders, each optimizing their own sleeve.

In total-fund models, staff spend more time discussing cross-portfolio effects:

“If we add this private strategy, what factor exposure are we already carrying elsewhere?”

“Does this credit position duplicate risk we already have through equity cyclicals?”

“Are we paying twice for the same macro bet?”

These are better questions, and they usually lead to cleaner portfolios.

Even when teams disagree, the disagreement is productive because everyone is scoring against one shared objective.

Beneficiaries have a different experience: trust.

Most members are not asking for a seminar on benchmark construction.

They want to know whether retirement promises are credible, contribution policy is responsible, and communication is honest.

Systems that explain results clearlyespecially after tough periodsbuild legitimacy.

Systems that hide behind complexity lose it.

In this sense, simplicity is not merely an investment technique; it is a public trust strategy.

The most useful takeaway from these real-world experiences is straightforward:

simple governance improves behavior.

It shortens decision cycles, clarifies accountability, and lowers the chance that expensive complexity survives on inertia.

For CalPERS, that means the “simpler approach” should be treated as an operating discipline, not a branding line.

Keep what works, cut what doesn’t, and publish the evidence.

If done well, members get stronger retirement security, employers get better predictability, and taxpayers get fewer fiscal surprises.

That is what successful simplification feels like on the ground.