Table of Contents >> Show >> Hide

Ah, the stock market: it’s zooming higher, investors are popping champagne corks over record-high indices, and everyone wants in. But behind the glitzcould we be dancing on the edge of a bubble? In this article, we’ll poke into the valuation textbooks, survey what market strategists are whispering behind closed doors, and try to answer whether this current surge is a sustainable bull run… or a bubble waiting to burst.

What’s fueling the boom?

Over the past year the U.S. stock market has surged in spite of cross-winds: geopolitical uncertainty, stubborn inflation, and a central bank that could still tighten. One of the key engines? The hype around artificial intelligence (AI). Companies like Nvidia and other tech heavyweights have seen meteoric rises, buoying broad indexes in the process.

Here are some of the main drivers:

- Transformative tech optimism. Investors are betting that AI isn’t just a fad, but a generational change. That promise has helped push valuations upward.

- Low interest rates and loose money (historically speaking). When bonds yield less, stocks look comparatively attractive, so capital flows. Though rates are higher than pandemic-era lows, the mindset remains: growth is king.

- Concentration of gains. A handful of mega-cap stocks now dominate the market’s returns, meaning the boom is less broad than it appears.

- Strong corporate earnings (so far). Unlike some previous bubbles where profits were speculative or absent, many of today’s tech winners are generating real cash flowthough the question is how far out their earnings can go.

When does a boom become a bubble?

Before we don our warning signs helmet, let’s define terms. A “bubble” typically means asset prices have detached from fundamentalsprofitability, cash flow, reasonable growthand are instead driven by the belief that prices will just keep going up because someone else will buy at a higher price tomorrow.

Classic characteristics of a bubble often include:

- Sky-high valuations compared with historical norms.

- Leverage or credit driving the surge (borrow-to-invest).

- Massive speculative entriesinvestors chasing hype rather than fundamentals.

- Rapid expansion of an industry or theme (think: internet in the late 1990s) ahead of actual profit realisation.

- A trigger or loss of faith that prompts a sharp correction.

Are those signs present today?

Let’s check one by one:

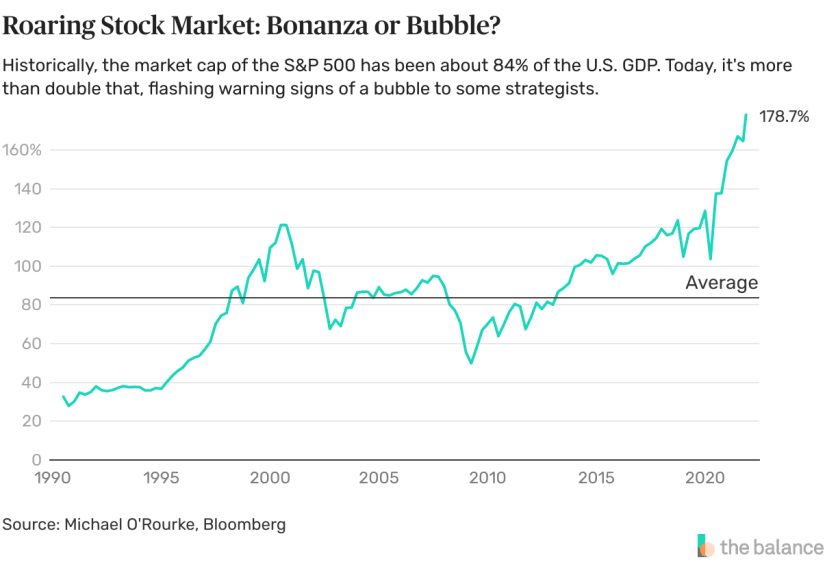

- Valuations? Yes. Many analysts point out metrics such as the cyclically adjusted P/E (CAPE) ratiootherwise known as the Robert Shiller P/Ehave surged to levels last seen around the dot-com peak.

- Leverage/concentration? There is concern. A small group of tech giants command an outsized share of the market’s value, meaning the risk is less diversified. However, the broad economy isn’t yet awash in reckless borrowings the way past bubbles were.

- Speculative entries? Some yespockets of unprofitable companies or hyper-growth stories with thin earnings are drawing attention. But the bulk of gains remain concentrated in profitable firms.

- Industry explosion ahead of profit? Possiblyespecially in infrastructure around AI (data centers, chips, etc.). The question: will the profits justify the investment? Some strategists say maybe not.

In short: yes, many warning lights are blinkingbut that doesn’t automatically guarantee a crash.

The other side: Why it might not be a classic bubble

Here’s the cheerleader half of the argument:

- Real profits exist. Unlike many historical bubbles (e.g., dot-com), many of today’s technology players are already showing earnings and cash flow, which lends support to valuations.

- Better financial discipline. Many large firms are carrying less debt, and capital spending is more internally financedso the risk of leverage-induced collapse is lower.

- Different structure, different era. Some analysts argue that comparing today to 2000 is apples to oranges: the global economy, regulation, investor base, and technology are meaningfully different.

- Valuations may feel high but not yet extreme. For example, a major bank’s note suggested valuations “stretched but not yet at historical bubble levels”.

So, might the boom continue? Possiblybut with caveats.

Key risk triggers to watch

Even if this isn’t an obvious bubble, risks abound. Consider keeping an eye on:

- Earnings disappointment. If the AI narrative falters (lower growth, fewer efficiencies realised), valuations could snap back.

- Interest-rate or liquidity shock. A sudden tightening of monetary policy, or a failure to cut rates when expected, could prick the boom. Many investors assume rates stay lowif they’re wrong, ouch.

- Competitive/technological risk. If the promise of AI doesn’t scale as fast or as profitably as hoped, many bets will be wasted.

- Concentration risk. With so much of the market value in a few names (the “Magnificent 7” for example), any stumble there could drag broader indices.

So … is it a bubble?

If I were wearing my fortune-teller hat (with a side of humor), I’d say: *maybe, but not yet explosive*. The market shows many of the features of a bubbleincluding frothy valuations and enthusiastic flowsbut it hasn’t yet ticked all the classic boxes (runaway leverage, mass speculative mania, broad-based collapse risk). The jury is out.

If you’re an investor reading this, here’s the takeaway: the boom could stretch a bit further, but this is not the time to pretend you’re invincible. Diversification matters, keep tabs on fundamentals, and don’t assume gravity takes a holiday.

Wrap-Up in Plain English

The U.S. stock market’s recent rally is powered by big themesespecially AIand strong earnings from top firms. Sure, valuations are high, and yes, some parts of the market are behaving like they’ve had too many cups of investor coffee. But unlike past bubble implosions, the foundations here are relatively sound. That doesn’t mean the rooftop party won’t end eventuallyjust that the wrecking ball isn’t swinging yet. Stay smart, stay diversified, and maybe keep one eye on the exit.

Meta Info for the Publishing Machine

Additional : Experiences Related to the Topic

Now, let’s shift gears and get a little personal because all the charts and metrics in the world don’t replace the human experience of investing, riding the highs, and coping with the scares.

I remember back in the late 1990s, I was fresh out of college and chided my grandparents for missing the “Internet wave.” My friend Jeremy bought shares of a company that made “interactive web pets” (yes, you read that right) because “the future is totally digital bro.” We watched the share price leap, his ego inflate, and then *poof*months later he was moaning about how he “lost more than I made in all of college.” Classic bubble behavior.

Fast-forward to more recently. A few years ago I dipped into a “hot” tech IPO because the hype cycle was so insane. The day after I half-heartedly justified it (“Hey, this company will revolutionize everything!”), the price stalled. My internal barometer of “hype > earnings” kicked in I jettisoned the position, took a small loss, and learned the lesson: just because the narrative is shiny doesn’t mean the profit is real.

This time around, as I watch friends and colleagues talk up AI stocks with gleeful abandon (“This will be like Amazon in 1997!”), I feel the same tingle of “Waita-minute.” When conversations shift from “What this company makes” to “What this company *could* make if everything goes right,” my bubble-alert lights start flashing. Yet at the same time, I’m seeing real companies delivering results, so I’m not panicking yet.

Here’s how I’m managing it personally:

- I’m making sure that the cornerstone of my portfolio is built on companies with earnings, cash flow, and a business model I can explain out loud without coughing nervously.

- I’m limiting exposure to the “story stocks” the ones with a brilliant vision and no profits because those are the ones that tend to get whacked when mood changes.

- I’m scenario-planning: What if the market turns? What if rates go up and liquidity dries? What if AI takes longer than expected to pay off? I’m asking “What if” more than “What now.”

- I remind myself: even if it’s *not* a bubble, history shows that valuations at the high end tend to lead to lower returns in the future. So I’m tempering my expectations.

In my discussions with smaller investors folks saving for a house, retirement, kids’ college I emphasize: don’t get left chasing the headlines. The story may be sexy, but if you buy at the top of the hype and the results come slower than hoped, you’ll feel it. Time in the market matters, but time in the right type of market (with some value and guardrails) matters *more*.

In short: I’m not hiding under the bed waiting for a crash, but I keep the emergency exit in mind. I’m enjoying the party, but I’m not leaving my glasses unattended. Because whether this boom becomes a full-blown bubble or just a high peak in a decent bull run, the steward of my capital isn’t the narrator of the hype it’s my own checklists and scenario plans.

And when the music stops sooner or later it always does I’ll be ready to sit down, take a sip of water, and wait for the next wave rather than scrambling to find the life raft.